Niger’s Financial Struggles Cast Shadow Over UEMOA Banking Sector

The January 2026 economic outlook report for the West African Economic and Monetary Union (UEMOA) reveals a troubling divide within the region’s banking system. While overall credit volumes have surged to a historic 40.031 trillion CFA francs—a 4.7% year-on-year increase—the sector faces mounting pressure from soaring non-performing loans (NPLs). At the epicenter of this instability, Niger stands out with the highest deterioration rate in the union, signaling deeper structural vulnerabilities.

Niger: A Regional Outlier in Financial Instability

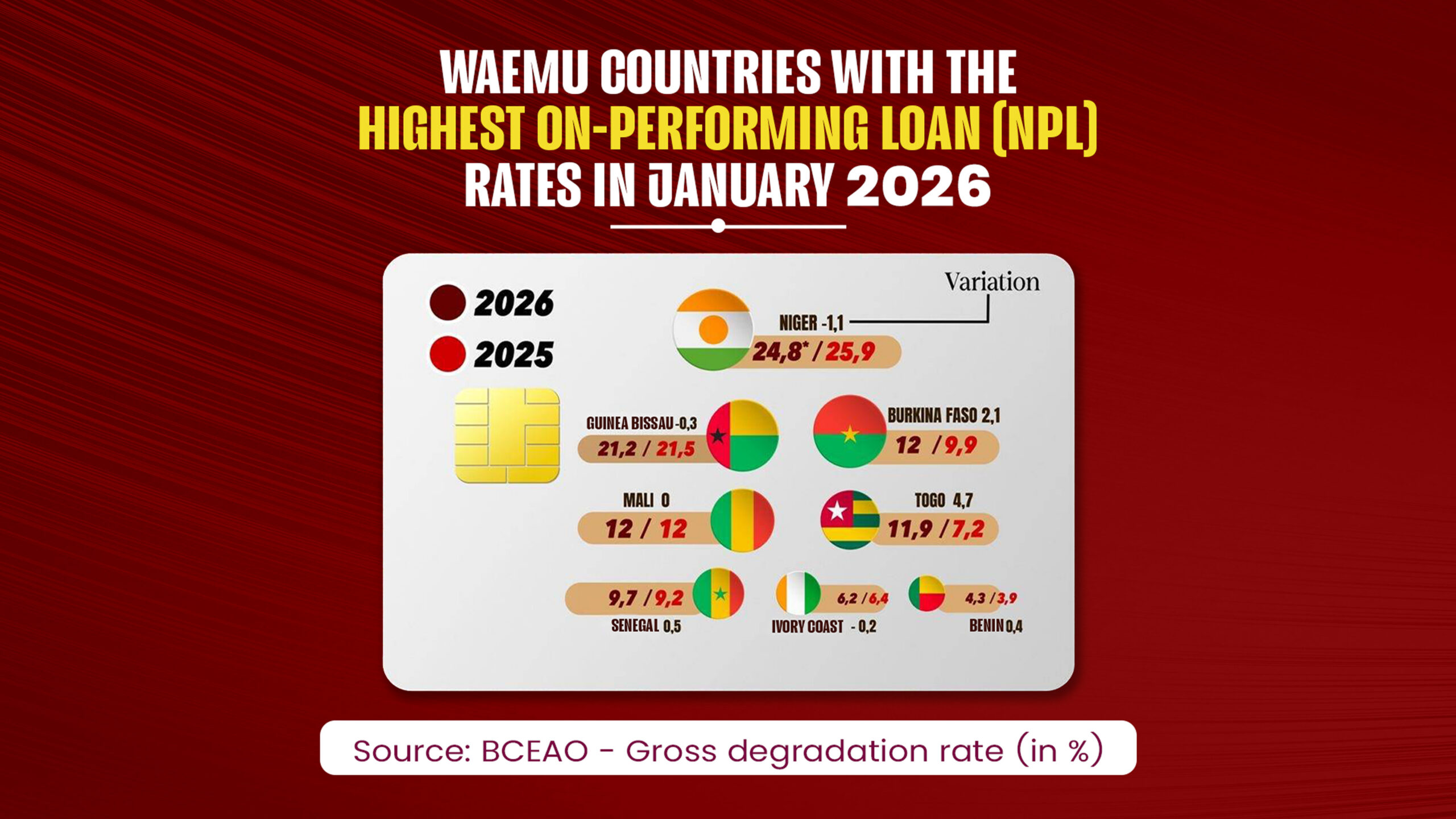

Despite marginal improvements, Niger remains the most fragile link in UEMOA’s banking chain. The country’s NPL ratio reached 24.8% in January 2026, meaning nearly one in four loans issued in Niger are in default. While this represents a slight decline from 25.9% in 2025, the gap between Niger and the regional average underscores a disproportionate exposure to risk, exacerbated by security challenges and political instability.

A Divided Union: Coastal Nations vs. Sahel States

The latest data underscores a stark economic divide within UEMOA, separating the relatively stable coastal economies from the crisis-hit Sahel belt, where Niger’s struggles are most pronounced.

The Sahel’s Growing Financial Stress

- Mali and Burkina Faso: Both nations report NPL rates of 12%, with Burkina Faso experiencing a sharp 2.1-point increase over the past year.

- Guinea-Bissau: The country remains in critical territory with a 21.2% NPL rate, second only to Niger.

Coastal Economies Show Greater Resilience

In contrast, most coastal UEMOA members demonstrate stronger loan portfolios, though not without concerns:

- Benin: Leads the region with the lowest NPL rate at 4.3%.

- Côte d’Ivoire & Senegal: Maintain relative stability with rates of 6.2% and 9.7%, respectively.

- Togo: A notable exception, with NPLs surging from 7.2% to 11.9% (+4.7 points) in a single year.

Systemic Risks Threaten Regional Banking Stability

The total NPL volume in UEMOA has ballooned to 3.631 trillion CFA francs, pushing the coverage ratio—a measure of banks’ ability to absorb losses—to just 59%. This erosion of financial buffers raises alarms about the sector’s ability to weather further shocks.

Banks are responding by tightening lending standards, including higher down payment requirements and stricter collateral demands. While these measures aim to mitigate risk, they risk choking off credit access for small and medium-sized enterprises (SMEs), which are vital to regional economic growth.

2026: A Pivotal Year for UEMOA’s Financial Future

As the union grapples with Niger’s outsized burden and the spread of financial stress in the Sahel, the banking sector hangs in a precarious balance. Though the system’s overall resilience has not yet been broken, the warning signs are undeniable. Policymakers and financial institutions face a critical challenge: preventing localized crises from spiraling into a liquidity crunch with regional consequences.